The real estate landscape is constantly evolving. As we look toward the horizon of 2026, homeowners and prospective buyers in Woodhaven and the greater Downriver area are asking the same question: “What is the smartest move for my financial future?” Whether you are looking to purchase your first home, upgrade to a larger property, or leverage your current equity, success in the 2026 housing market requires foresight, strategy, and a trusted local partner.

At Mortgage 1 Downriver, we believe that an educated borrower is an empowered borrower. Led by Joseph Migliaccio, our team has helped thousands of families navigate the complexities of home financing. This comprehensive guide serves as your strategic roadmap for mortgage planning in 2026, specifically tailored for our neighbors here in Michigan.

Why Strategic Mortgage Planning Matters in 2026

Gone are the days when you could simply look at a house on a Saturday and close a loan effortlessly on a Monday without preparation. The economic climate of the mid-2020s has introduced new variables regarding interest rates, housing inventory, and lending guidelines. Planning for 2026 isn’t just about finding a house; it is about architectural financial planning.

A solid mortgage plan helps you:

- Lock in favorable terms: Understanding rate trends allows you to time your lock effectively.

- Strengthen purchasing power: Proper debt management can significantly increase the amount you qualify to borrow.

- Avoid closing delays: Pre-emptive document gathering streamlines the underwriting process.

- Compete in a local market: In Woodhaven and Downriver, desirable homes move quickly. A solid financial backbone makes your offer stand out.

The Woodhaven & Downriver Real Estate Landscape

Real estate is hyper-local. While national headlines might predict doom and gloom or skyrocketing booms, the reality in Woodhaven, MI, is often more nuanced. The Downriver community remains a robust market for families looking for value, community, and accessibility. However, inventory constraints have made it essential for buyers to be fully prepared before entering the market.

As a local lender voted Downriver’s #1 Mortgage Lender for over a decade, we understand the specific appraisal quirks, property taxes, and neighborhood values that national online lenders simply miss. When you work with Mortgage 1 Downriver, you aren’t just getting a loan; you are getting a localized strategy.

Your 2026 Mortgage Roadmap: A Quarterly Guide

To help you prepare, we have broken down the year into actionable phases. Whether you are planning to buy in Spring 2026 or refinance in the Fall, follow this timeline to ensure success.

Phase 1: The Financial Health Check (3-6 Months Before Buying)

Before you ever scroll through listing photos, you must look at your financial reflection. This phase is dedicated to cleaning up your credit and accumulating capital.

- Review Your Credit Report: Pull your reports from the major bureaus. Dispute any errors immediately. In 2026, credit score tiers are more segmented than ever, meaning a 20-point swing can impact your interest rate significantly.

- Calculate Debt-to-Income (DTI) Ratio: Lenders look closely at how much of your monthly income goes toward debt payments. Try to pay down high-interest credit cards to lower this ratio.

- Determine Your Budget: Use our tools to calculate your payment scenarios. Remember to factor in Michigan property taxes and homeowners insurance, not just principal and interest.

Phase 2: Pre-Approval & Team Building (1-3 Months Before Buying)

This is where the rubber meets the road. A pre-qualification is a good estimate, but a Pre-Approval is a verified commitment that sellers respect.

During this phase, you should meet with Joseph Migliaccio to discuss your goals. We will verify your income, assets, and employment to issue a strong pre-approval letter. This is also the time to understand the Purchase Process in detail so there are no surprises.

Phase 3: The Hunt & The Offer (The Active Phase)

With your pre-approval in hand, you are ready to tour homes in Woodhaven. Because you have completed the hard work in Phases 1 and 2, you can move with speed.

- Stay within your limits: Just because you are approved for a certain amount doesn’t mean you must spend it all. Stick to the monthly payment budget we established together.

- Local Expertise: Lean on your real estate agent to find pockets of value in the Downriver area.

- Make a Strong Offer: Your Mortgage 1 pre-approval signals to the seller that your financing is secure, often giving you an edge over buyers using big-box internet lenders.

Refinancing in 2026: Is It Time to Tap Your Equity?

Mortgage planning isn’t just for homebuyers. If you already own a home in Woodhaven, 2026 might be the year to restructure your debt. Home values in Michigan have seen steady appreciation, meaning you likely have significant equity.

Consider refinancing if:

- You want to consolidate debt: High-interest credit card debt can be rolled into a lower-interest mortgage, potentially saving you hundreds per month.

- You need to fund renovations: Love your location but need a modern kitchen? A cash-out refinance can fund the project.

- You want to remove PMI: If your home value has risen enough to give you 20% equity, you might be able to eliminate Private Mortgage Insurance.

Learn more about how our team handles the Refinancing Process to see if it makes financial sense for you.

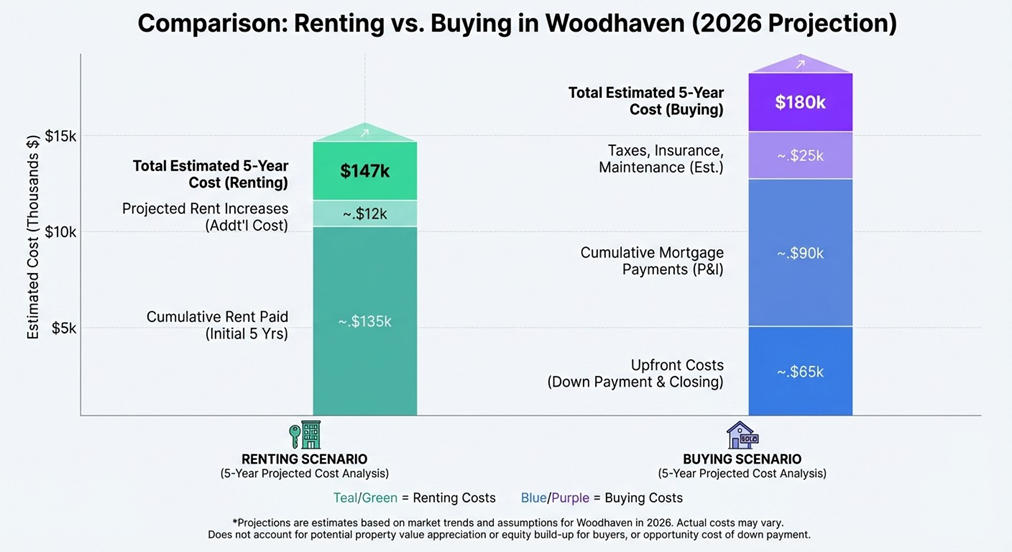

Comparison: Renting vs. Buying in Woodhaven (2026 Projection)

Factor Renting Buying (Mortgage 1 Plan) Monthly Payment Stability Subject to annual increases (Inflation/Landlord discretion). Fixed-rate principal and interest payments remain stable for 15-30 years. Equity Building $0. You are paying your landlord’s mortgage. Every payment reduces your debt and builds ownership wealth. Tax Benefits None. Potential deductions for mortgage interest and property taxes (consult your tax advisor). Customization Limited. Permission required for changes. Full control. Renovations can increase property value. 5-Year Net Cost High (100% unrecoverable cost). Lower (Cost is offset by appreciation and principal reduction).

Why Choose a Local Broker Over a Big Bank?

In an era of automated approvals and AI chatbots, the human element of mortgage lending is more valuable than ever. Mortgage 1 Downriver offers a distinct advantage over national banks.

1. Speed and Agility

2. Product Variety

As a broker, we have access to a wide variety of loan products, including FHA, VA, USDA, Conventional, and specialized programs for first-time buyers. We shop the market for you to find the best rate and terms for your specific situation.

3. Availability

Frequently Asked Questions (FAQs)

1. How early should I start the mortgage process for a 2026 purchase?

We recommend starting the conversation at least 3 to 6 months before you plan to buy. This gives us ample time to review your credit, correct any errors, and determine a comfortable budget.

However, we can also expedite the process if you find a home unexpectedly.

2. What is the minimum down payment required in Michigan?

Many buyers believe they need 20% down, but that is a myth. Qualified buyers can purchase a home with as little as 3% down on conventional loans, or 3.5% for FHA loans. VA loans and USDA Rural Development loans may even offer 0% down payment options for eligible borrowers and properties.

3. How do interest rates affect my purchasing power?

Interest rates directly impact your monthly payment. A higher rate reduces the total loan amount you qualify for to keep the payment within your debt-to-income limits. We help you strategize by looking at different rate scenarios and discussing “buydown” options to lower your rate temporarily or permanently.

4. Can I get a mortgage if I am self-employed?

Absolutely. While self-employed borrowers may need to provide additional documentation (such as tax returns or bank statements) to prove income stability, Mortgage 1 specializes in helping business owners in Woodhaven secure financing.

5. What makes Mortgage 1 Downriver different from other lenders?

We are deeply rooted in the Downriver community. With billions in closed mortgages and over a decade of being voted the #1 lender in the area, our reputation is built on trust, transparency, and results. We treat every client like a neighbor because, in many cases, you are.

Ready to Build Your 2026 Mortgage Plan?

The best time to plant a tree was 20 years ago; the second-best time is now. The same logic applies to your mortgage planning. Don’t wait for the market to dictate your future—take control of your homeownership journey today.

Whether you are looking to buy your first home in Woodhaven, upgrade your current living situation, or refinance for financial freedom, Joseph Migliaccio and the Mortgage 1 team are here to guide you every step of the way.