Breaking the 20 Percent Myth for Woodhaven Homebuyers

For decades, prospective buyers have been told they need a massive twenty percent down payment to purchase a home. As we look ahead to 2026, this outdated advice is keeping many qualified families from achieving their homeownership dreams. At Mortgage 1, Downriver, we are here to set the record straight for residents in Woodhaven, MI and the surrounding communities.

The truth is that modern purchase processes offer incredible flexibility. Whether you are a first-time buyer or looking to upgrade your current living situation, there are numerous loan programs designed to minimize your upfront costs. Here are a few reasons why a smaller down payment might make sense for you:

- Preserving cash reserves: Keep more money in your bank account for emergencies, renovations, or furnishing your new home.

- Entering the market sooner: Stop paying rent and start building equity without waiting years to save a massive lump sum.

- Leveraging special programs: Take advantage of state and local grants specifically designed for homebuyers in Michigan.

If you have been holding off on starting your home search because of down payment concerns, it is time to explore your actual options with Downriver’s number one mortgage lender.

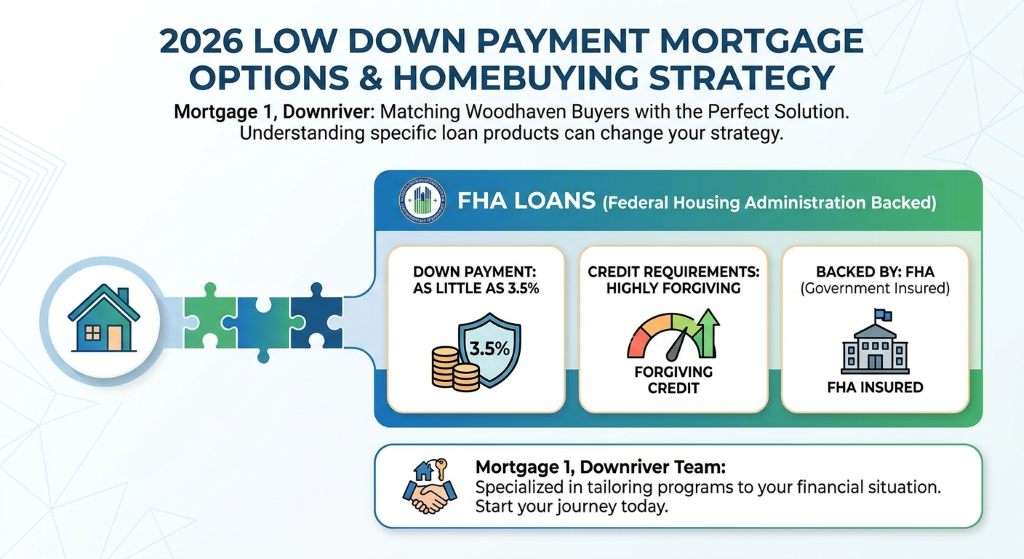

Top Low Down Payment Mortgage Programs in 2026

Understanding the specific loan products available can completely change your homebuying strategy. In 2026, lenders offer a variety of programs tailored to different financial situations. Our team at Mortgage 1, Downriver specializes in matching Woodhaven buyers with the perfect mortgage solution.

Here is a closer look at the most popular low down payment options:

- FHA Loans: Backed by the Federal Housing Administration, these loans require as little as 3.5 percent down and are highly forgiving of lower credit scores.

- VA Loans: Exclusive to eligible veterans and active-duty military personnel, VA loans offer a phenomenal zero down payment option with no private mortgage insurance requirement.

- USDA Loans: Designed for rural and some suburban areas, USDA loans also allow for zero percent down. Certain areas around Michigan may qualify, making this a fantastic option for eligible buyers.

- Conventional Loans: First-time homebuyers can often secure a conventional mortgage with just 3 percent down, provided they meet specific credit and income requirements.

By exploring these pathways, you can stop stressing about saving twenty percent and start focusing on finding the perfect property.

| Loan Type | Minimum Down Payment | Credit Score Requirement | Ideal Borrower Profile |

|---|---|---|---|

| VA Loan | 0% | Flexible (Typically 620+) | Veterans and active-duty military |

| USDA Loan | 0% | 640+ | Buyers in eligible rural/suburban areas |

| Conventional Loan | 3% | 620+ | First-time buyers with good credit |

| FHA Loan | 3.5% | 580+ | Buyers needing flexible credit guidelines |

| Traditional Conventional | 5% to 20% | 620+ | Repeat buyers or those with larger savings |

How to Prepare Your Finances for a 2026 Home Purchase

Getting ready to buy a home requires more than just saving for the down payment. It involves optimizing your entire financial profile to ensure you get the best possible interest rate and terms. As your local Woodhaven mortgage experts, we recommend taking a proactive approach to your homebuying journey.

Start by reviewing your credit report for any errors and paying down high-interest debt. Next, gather your financial documents, including recent pay stubs, W-2s, and bank statements. Having these ready will streamline the pre-approval process.

Most importantly, partner with a knowledgeable local lender. Joseph Migliaccio and the experienced team at Mortgage 1, Downriver have been voted the top lender in the area for eleven years in a row. We understand the local Michigan market and can help you navigate down payment assistance programs that you might not even know exist. If you are wondering how much you can afford, we can run the numbers together and build a customized roadmap to homeownership.

Q1: Do I really need a 20 percent down payment to buy a home in Woodhaven?

Absolutely not. While a 20 percent down payment eliminates the need for private mortgage insurance, many buyers successfully purchase homes with as little as 0 to 3.5 percent down using VA, USDA, FHA, or Conventional loan programs.

Q2: Can I use gift funds for my down payment in 2026?

Yes, most loan programs allow you to use financial gifts from family members to cover all or part of your down payment. You will just need a formal gift letter stating that the money does not need to be repaid and was not a loan.

Q3: What is down payment assistance and do I qualify?

Down payment assistance programs provide grants or secondary loans to help cover upfront costs. Eligibility usually depends on your household income, the home’s location, and whether you are a first-time buyer. Our team at Mortgage 1, Downriver can help determine your eligibility for Michigan-specific programs.

Q4: How do I know which loan program is best for my financial situation?

The best way to choose a loan program is to consult with an experienced mortgage professional. We will review your credit score, income, savings, and homeownership goals to recommend the most cost-effective option for your specific needs.

Q5: How can I get started with Mortgage 1, Downriver?

Getting started is easy! You can reach out to Joseph Migliaccio directly by calling 1-734-341-4322 or emailing jmigliaccio@mortgageone.com to schedule your free consultation and begin the pre-approval process.Get Pre-Approved Today with Mortgage 1, Downriver