Navigating the 2026 Mortgage Market in Woodhaven, MI

As we step into 2026, the real estate market in Woodhaven, MI, continues to present unique opportunities for prospective homebuyers. Whether you are a first-time buyer or looking to upgrade your current residence, choosing the right financing option is critical to your long-term financial health. At Mortgage 1, Downriver, we understand that navigating the myriad of loan products can feel overwhelming.

Led by Joseph Migliaccio, our team is dedicated to helping you compare FHA, VA, and Conventional loans to find the perfect fit for your specific needs. Understanding the nuances of these mortgage programs will empower you to make an informed decision and secure your dream home in Wayne County.

Comparing FHA, VA, and Conventional Loan Programs

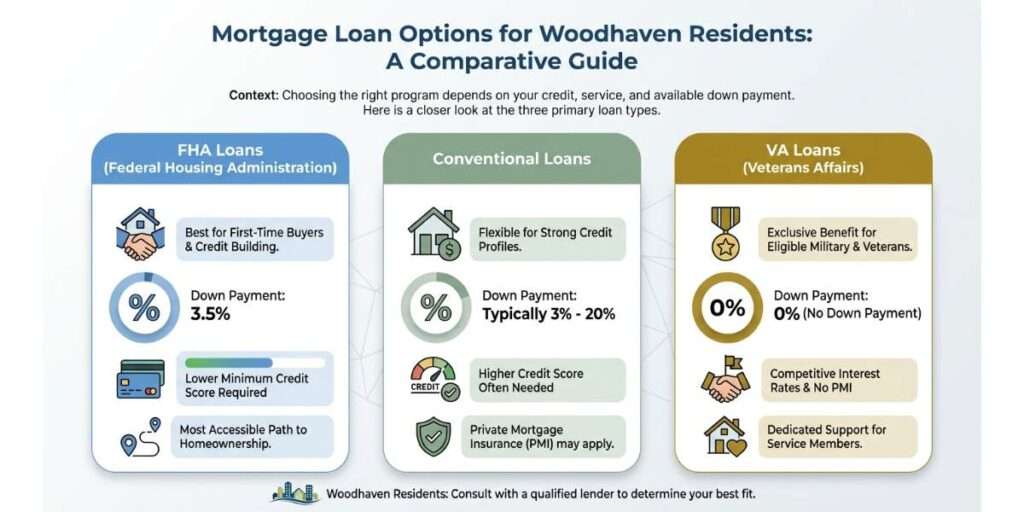

Each mortgage program offers distinct advantages depending on your credit history, military service, and available down payment. Here is a closer look at the three primary loan types available to Woodhaven residents:

- FHA Loans: Backed by the Federal Housing Administration, these loans are fantastic for first-time buyers. They typically require a lower minimum credit score and a down payment of just 3.5 percent. If you are building your credit, an FHA loan might be your most accessible path to homeownership.

- VA Loans: Available exclusively to eligible veterans, active-duty service members, and their spouses. Guaranteed by the Department of Veterans Affairs, these loans offer incredible benefits like zero down payment and no private mortgage insurance (PMI). We are proud to serve our local military families at our Woodhaven office.

- Conventional Loans: These are not insured by the federal government. They generally require a higher credit score but offer flexible terms and potentially lower interest rates for borrowers with strong financial profiles. A conventional loan is often the preferred choice for buyers who have saved a substantial down payment.

Consulting with a local expert like Joseph Migliaccio can help you weigh these options against your current financial reality and future goals.

| Loan Type | Min. Down Payment | Min. Credit Score (Typical) | PMI / Mortgage Insurance | Best For |

|---|---|---|---|---|

| FHA | 3.5% | 580 | Required (Upfront & Annual) | First-time buyers, lower credit |

| VA | 0% | No official minimum (varies) | None (Funding Fee applies) | Veterans & Active Military |

| Conventional | 3% to 5% | 620 | Required if down payment is under 20% | Good credit, larger down payments |

Making the Right Choice for Your Woodhaven Home

Choosing between an FHA, VA, or Conventional loan in 2026 ultimately depends on your unique financial picture. You must consider your credit score, how much cash you have saved for a down payment, and your long-term plans for the property. Working with a local lender ensures you receive advice tailored to the Woodhaven real estate market.

At Mortgage 1, Downriver, we take the time to review your financial documents and explain every detail of the mortgage process. Our goal is to secure a competitive rate and a comfortable monthly payment for you. Do not let the complexities of mortgage lending keep you from achieving your homeownership dreams this year.

Q1: What is the main difference between FHA and Conventional loans?

FHA loans are government-backed and cater to borrowers with lower credit scores, while Conventional loans are not government-insured and typically require stronger credit profiles.

Q2: Can I buy a home in Woodhaven with no down payment?

Yes, if you qualify for a VA loan or certain USDA programs, you can purchase a home with zero down payment.

Q3: Are interest rates lower for VA loans?

Generally, VA loans offer some of the most competitive interest rates on the market because they are backed by the government, which reduces the risk for lenders.

Q4: How do I know if I qualify for a mortgage in 2026?

The best way to determine your eligibility is to get pre-approved. Contact Joseph Migliaccio at Mortgage 1 Downriver to review your income, credit, and debt-to-income ratio.

Q5: Can I switch from an FHA loan to a Conventional loan later?

Absolutely. Many homeowners choose to refinance their FHA loan into a Conventional loan once they have built up 20 percent equity in their property to eliminate mortgage insurance premiums.

Call Joseph Migliaccio at Mortgage 1 Today